Implications of a Net-Zero Target for India’s Sectoral Energy Transitions and Climate Policy

Overview

This study presents alternative peaking and net-zero scenarios for India and highlights its implications for transition in the energy-intensive sectors such as electricity, transport, building, and industry. It explores four combinations of peaking and net-zero-year scenarios for India (2030–2050, 2030–2060, 2040–2070, and 2050–2080) and analyses how a combination of possible technological developments like carbon capture, utilisation and storage (CCUS) and hydrogen production would affect the transition within each of the policy scenarios. Further, the study presents sectoral pathways based on 16 policy-technology scenario combinations for the required sectoral transitions and provides insights into India’s climate policy.

Key Findings

- In the absence of CCS, India’s fossil fuel share in the primary energy mix would need to decline to 5 to 6 per cent in the net-zero year. However, the availability of CCS would allow a 19 to 30 per cent share of fossils in primary energy.

- In the net-zero year, across scenarios, without developments in hydrogen production and CCS, the share of e-trucks sales would increase to 100 per cent.

- By 2100, the share of solar in net-zero scenarios, without CCS and hydrogen, is estimated to be 70 to 72 per cent in total electricity generation. Similarly, the share of biofuels in the net-zero scenarios would be 80-83 per cent.

- In the presence of CCS, coal can hold a share of 3-5 per cent in primary energy in different net-zero scenarios but has to ultimately decline to around 1 per cent share.

- In a net-zero world, where CCS is unavailable, the carbon price is estimated to be higher than 900 USD (2015 prices)/tCO2. However, the availability of CCS could reduce the carbon price by half.

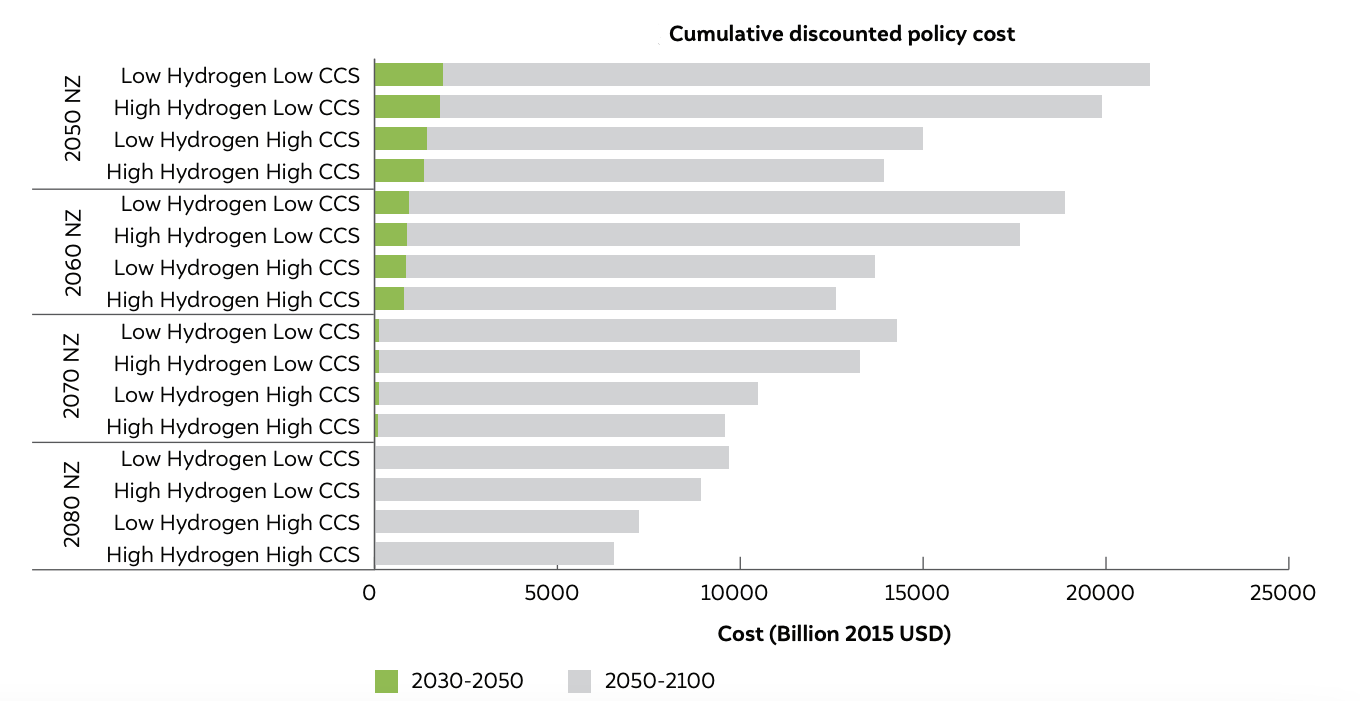

Policy cost across scenarios

Source: Authors’ analysis

- India’s power generation assets would need 3.72 per cent of total land area by 2050 if India decides to reach net-zero by 2050. Across all the scenarios, the increase in land area for power generation would be 4.92 to 6.09 per cent by 2100.

- The feasibility of net-zero transition would be determined by a vast range of factors, including per capita income, economic growth, availability and cost of mitigation technologies etc.

- Global financial assistance to developing countries like India is a must to meet their net-zero ambitions.

Following are the 12 critical milestones for the 2040 peaking–2070 net-zero scenario with no commercial availability of CCS but hydrogen being commercially available:

Note: The study presents many scenarios and does not recommend any of them. The intent is to highlight the range of possible futures for the country depending upon choices for peaking-net-zero and technology availability.

Power sector

- Coal-based power generation must peak by 2040 and reduce by 99 per cent between 2040 and 2060

- Solar-based electricity generation capacity must increase to 1689 GW by 2050 and 5,630 GW by 2070

- Wind-based electricity generation capacity much increase to 557 GW by 2050 and 1792 GW by 2070

- Nuclear-based electricity generation capacity must increase to 68 GW by 2050 and 225 GW by 2070

Transport sector

- The share of electric cars in car sales must reach 84 per cent by 2070

- The share of electric trucks in freight trucks must total 79 per cent by 2070, the rest being fuelled by hydrogen

- The share of biofuel blend in oil for cars, trucks, and airlines must touch 84 per cent by 2070

Industrial sector

- Coal use in the industrial sector must peak by 2040 and reduce by 97 per cent between 2040 and 2065

- Hydrogen share in total industrial energy use (heat and feedstock) must increase to 15 per cent by 2050 and 19 per cent by 2070

- The industrial energy intensity of total GDP must decline by 54 per cent between 2015 and 2050 and by a further 32 per cent between 2050 and 2070

Building sector

- The intensity of electricity use in the building sector with respect to total GDP must decline by 45 per cent between 2015 and 2050 and by another 2.5 per cent between 2050 and 2070

Refinery sector

- Crude oil consumption in the economy must peak by 2050 and decrease by 90 per cent between 2050 and 2070