Will the Real Lithium Demand Please Stand Up? Challenging the 1Mt-by-2025 Orthodoxy

Lithium prices have halved since 4Q 2017, driven by perceptions of oversupply in the market and, as a result, major producers are pulling back and re-assessing expansion plans. This boom-bust cycle is not healthy – it breeds more risk and uncertainty for investors. It reemphasizes why it is so important for the lithium industry to get demand forecasting right and grow supply accordingly.

Recently, some companies claim that a slowdown in EV sales in China due to a subsidy cut have resulted in slower growth than anticipated. However, China had been planning the cut to EV subsidies since 2016 and automakers already knew this. The trade war has contributed to a global slowdown in auto sales, which has amplified the slowdown in EVs, but no producer in the EV supply chain should be surprised. Last year, BNEF forecasted that China’s EV sales growth in 2019-2020 would be slower than in 2017-18, as automakers’ costs take time to catch up with the subsidy cut and consumer behavior adjusts.

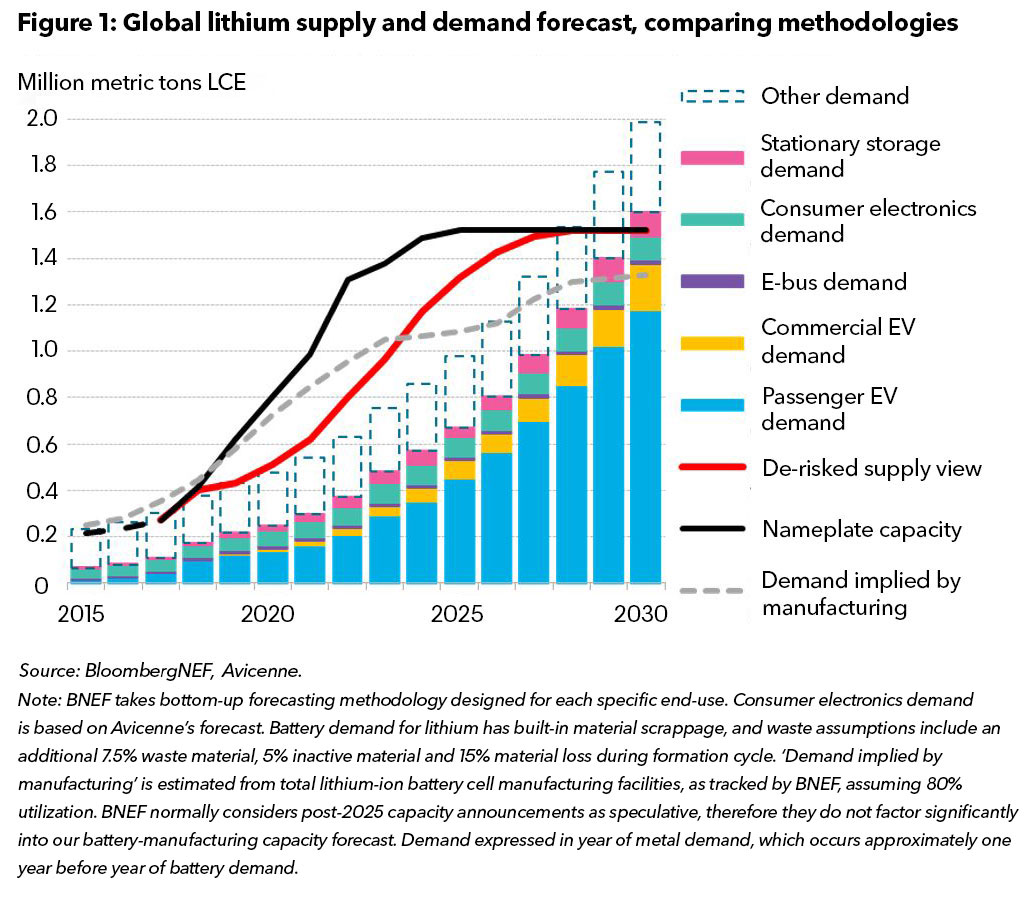

So what are the real reasons for the mismatch in expectations for growth between lithium producers and those in the EV market? Part of it may go back to underlying lithium-demand forecasting methodology. The dominant demand consensus amongst lithium producers in early 2018 was that battery demand for lithium chemicals would hit 1 million metric tons lithium carbonate equivalent (LCE) by 2025.

As illustrated by dotted grey-line in Figure 1 below, this may be true, if forecasting lithium demand is done with a top-down approach, estimating the amount of material needed by battery manufacturers according to how much capacity they are bringing online. However, this assumes that supply aligns with actual demand perfectly. In reality, you have multiple different battery manufacturers that are all expanding capacity to capture the same demand, in a race to gain market share. Therefore, the top-down approach of deriving lithium demand from battery manufacturing capacity has pre-2025 bias to overestimating the industry’s growth.

In contrast, BloombergNEF utilizes detailed bottom-up forecast methodology that reflects the unique growth drivers of each battery-market segment – we do not generalize. We forecast global lithium-ion battery demand will surpass 2,000 GWh by 2030. Key considerations for this bottom-up approach revolve around evolving consumer adoption rates, the changing pack size in vehicles, lithium content in chemistries, and the real-world cell energy densities.

We forecast battery demand for lithium chemicals will reach nearly 700,000 metric tons LCE by 2025. Adding around 300,000 metric tons LCE of non-battery lithium demand means global lithium resource demand could reach the famed “1 million metric tons LCE by 2025”. However, we emphasize that battery demand alone will not reach this target.

This compares to our forecast of 1.3 million metric tons of lithium resource de-risked mine capacity, and 915,000 metric tons of lithium chemical de-risked conversion capacity (45% carbonate, 55% hydroxide) by 2025. Although most of this chemical conversion capacity claims to be able to achieve battery-grade quality, we caution that 40% of this capacity is being developed by non-tier 1 producers so face headwinds in achieving quality and volume targets.

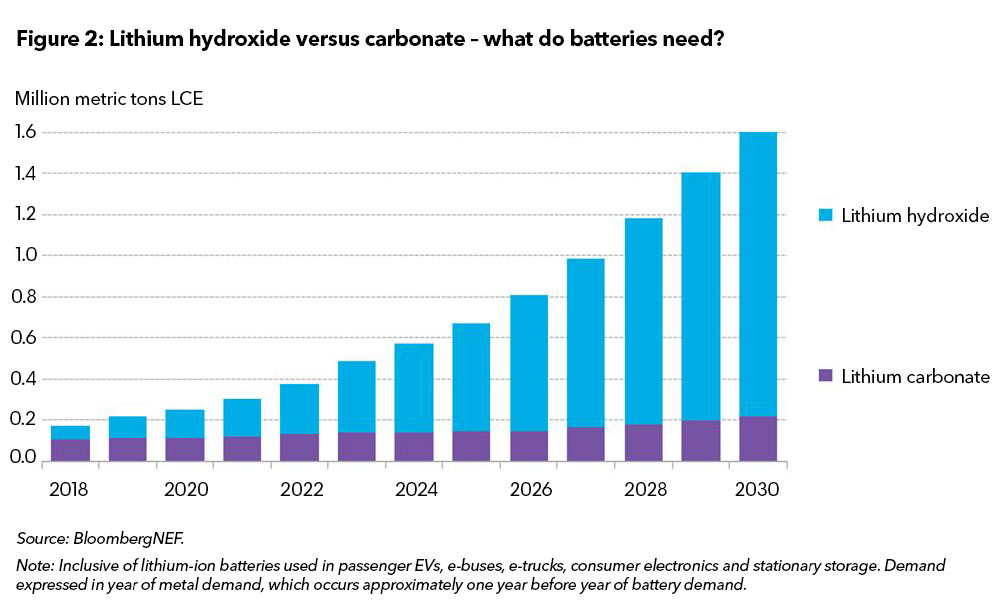

Another aspect of lithium-demand forecasts that has not yet achieved market consensus is the split between lithium hydroxide and carbonate. Again, utilizing our bottom-up forecasting, BloombergNEF projects that increasing adoption of higher-nickel cathode chemistries, particularly in passenger EV batteries, will drive demand for lithium hydroxide faster than carbonate. By 2030, demand for battery-grade lithium hydroxide will likely reach nearly 1.4 million metric tons LCE, while carbonate demand will reach 218,000 metric tons LCE in 2030. See Figure 2 below.

According to the refinery assets currently under development, as tracked by BloombergNEF, there may be an oversupply in lithium carbonate conversion capacity but a deficit of battery-grade lithium hydroxide by 2025. In a worst-case scenario, producers may be able to substitute hydroxide for carbonate in the production of medium nickel chemistries, such as nickel manganese cobalt (622).

Contact us to learn more about BloombergNEF forecasting in EVs, stationary storage, battery supply chain, and raw materials.

About BloombergNEF

BloombergNEF (BNEF), Bloomberg’s primary research service, covers clean energy, advanced transport, digital industry, innovative materials and commodities. We help corporate strategy, finance and policy professionals navigate change and generate opportunities.

Available online, on mobile and on the Terminal, BNEF is powered by Bloomberg’s global network of 19,000 employees in 176 locations, reporting 5,000 news stories a day.